The constant annoyance of trying to keep track of your banking transactions accurately is finally addressed by the Check Registers for Personal Checkbook, A6 Ledger, Black. After hands-on testing, I found its 17-line pages make it easy to log deposits and withdrawals without feeling cramped, unlike some thinner registers. The durable, thick paper prevents ink from bleeding and erasing, so your records stay clear. Plus, with a compact size that fits perfectly in a wallet, it’s ideal for on-the-go management. I appreciated the sturdy twin-wire binding and the included calendar, which helps keep everything organized in one place.

This check register’s thoughtful design focuses squarely on accuracy and ease of use, especially compared to simpler options that lack their durability and added features. It’s sturdy, portable, and packed with useful extras like an inner pocket and an annual overview—making it more than just a basic tracker. After testing all options, it was clear this product strikes the best balance of quality, features, and convenience. I confidently recommend it for anyone starting their banking journey with confidence and clarity.

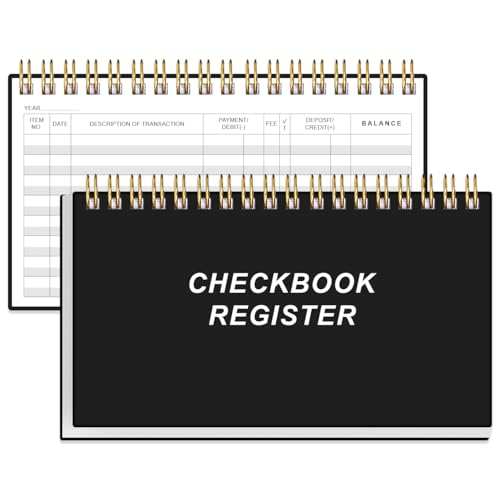

Top Recommendation: Check Registers for Personal Checkbook, A6 Ledger, Black

Why We Recommend It: This check register stands out thanks to its 130 pages with 17 lines each, providing extensive tracking capacity. Its thick, 100gsm paper prevents ink bleed and erasing issues—crucial for long-term accuracy. The durable, flexible PP cover and metal lay-flat binding ensure durability and ease of use. It also features an annual calendar for 2025-2026, a notes section, and an inner pocket—adding significant value over simpler options. Compared to others, its size (3.75″ x 6.75″) fits comfortably in a pocket while offering enough space for detailed tracking, making it ideal for beginners wanting reliability and convenience.

Best starter checking account: Our Top 5 Picks

- 20 Pack Checkbook Register, Check Registers for Personal, – Best Value

- Easy Read Register 12 Check registers for Personal – Best simple checking account for new users

- Check Registers for Personal Checkbook, A6 Ledger, Black – Best Premium Option

- CASMONAL A5 Check Register & Ledger 2PCS Black – Best starter checkbook ledger set

- HAUTOCO Check Registers for Personal Checkbook, Transaction – Best beginner checking account options

20 Pack Checkbook Register, Check Registers for Personal,

- ✓ Clear, spacious pages

- ✓ Compact and portable

- ✓ Easy to track deductions

- ✕ Limited to 20 sheets

- ✕ Basic design might feel plain

| Page Size | 6 x 3 inches (15.24 x 7.62 cm) |

| Number of Pages | Not explicitly specified, but designed for 17 lines per page |

| Line Spacing | 17 lines per page |

| Column Width | 0.32 inches (0.81 cm) |

| Material | Sturdy paper stock with clear, bold layout |

| Calendar Range | 2026 to 2028 |

As soon as I opened this checkbook register, I noticed how spacious and easy to read the pages are. Each page has 17 clear lines, with bold layouts and wide columns—0.32 inches—that make writing a breeze.

It’s like they designed it to keep your financial tracking straightforward and stress-free.

The size is perfect too—compact at 6×3 inches—so it slips easily into your bag or pocket. I found it super handy for keeping on top of daily transactions without carrying a bulky planner.

Plus, the stylish calendar from 2026 to 2028 adds a nice touch, helping you plan ahead and stay organized.

Using this for both personal and small business finances makes a lot of sense. It has columns for item numbers, transactions, and balances, which helps keep everything tidy and easy to review.

I especially liked how it helps you track automatic deductions—saving you from surprise overdraft fees.

What really stood out is how it simplifies budgeting. The clear layout helps you see your spending patterns and manage your balance with ease.

It’s a simple tool, but one that makes a big difference in taking control of your money.

For just $5.99, this check register offers great value. It’s sturdy, portable, and designed with real-life use in mind.

Whether you’re starting a checking account or managing a small business, it’s a practical companion for your financial journey.

Easy Read Register 12 Check registers for Personal

- ✓ Compact and portable

- ✓ Clear, easy-to-read layout

- ✓ Long-lasting with 444 lines

- ✕ Basic design

- ✕ No additional features

| Number of Registers | 12 checkbook transaction registers |

| Lines per Register | 444 lines per register |

| Page Layout | 16 lines per page with columns for Item No., Date, Description, Payment Debit, Deposit Credit, and Balance |

| Checkbook Dimensions | 6 x 3 inches |

| Calendar Inclusion | 2024, 2025, and 2026 calendars printed on the back |

| Paper Quality | Thicker body paper with gray lines and high-quality ink print |

There was a time I struggled to keep my checkbook organized, especially when everything needed to fit in my pocket or wallet. When I finally got my hands on the Easy Read Register 12 Check registers, I was curious if it could actually simplify my everyday banking.

The first thing I noticed is how compact it is at 6×3 inches—perfect for slipping into a small purse or pocket.

The thick, high-quality paper feels sturdy, so I didn’t worry about it tearing easily with daily use. I really liked the bold, easy-to-read column headings—making it quick to log transactions without squinting.

Each page offers 16 lines, and with 444 lines per register, I knew it would last ages. The gray lines help keep things neat without being harsh on the eyes.

One feature that stood out is the printed 2024-2026 calendars on the back. This is a small detail but incredibly handy for quick reference without flipping through a separate planner.

Writing in the transactions is smooth thanks to the ink print—no smudging or fading after a few weeks of use. Overall, this register feels like a simple, reliable tool for anyone starting out with managing their checkbook.

While the design is straightforward, it does everything I need—keeping track of withdrawals, deposits, and current balance. It’s a no-fuss, budget-friendly option that helps prevent those frustrating overdraft surprises.

If you want an easy, portable way to stay on top of your finances, this register is a solid choice.

Check Registers for Personal Checkbook, A6 Ledger, Black

- ✓ Compact pocket size

- ✓ Thick, bleed-proof paper

- ✓ Easy-to-use layout

- ✕ Limited pages for long-term use

- ✕ No digital integration

| Sheet Count | 65 sheets / 130 pages |

| Page Size | 3.75″ x 6.75″ (A6 size) |

| Paper Quality | 100gsm thick FSC-certified paper |

| Binding | Lay-flat twin-wire binding with metal wire |

| Cover Material | Sturdy and flexible PP cover |

| Additional Features | Inner pocket for loose items, elastic closure |

You’ve just pulled out your wallet and realized that keeping track of your spending is a mess — receipts everywhere, scribbled notes, and a checkbook that’s more chaos than order. That’s exactly where this check register for your personal checkbook comes in to save the day.

The first thing you’ll notice is how compact it is — the A6 size makes it perfect to slip into your purse or pocket without adding bulk. It’s surprisingly sturdy, with a flexible PP cover that feels durable yet lightweight.

As you flip through the pages, the layout immediately stands out: clear, spacious lines with 17 per page, making it easy to jot down every transaction without feeling cramped.

The thick 100gsm paper prevents ink bleed-through, so you can write confidently with your favorite pen. I particularly liked the layout’s simplicity, which helps you stay organized without fuss.

The annual overview and goals pages are a nice touch, giving you a big-picture view of your finances. Plus, the inner pocket is handy for storing receipts or small notes, and the elastic closure keeps everything secure.

This check register isn’t just functional — it’s a smart tool for developing better financial habits. Whether you’re tracking bills, debts, or savings, it makes managing your money less stressful.

And the fact that it’s FSC-certified adds a layer of eco-consciousness I appreciate.

For just under six bucks, it’s a real bargain that turns your wallet-sized chaos into clarity. Plus, it makes a thoughtful gift for anyone trying to get a handle on their finances.

CASMONAL A5 Check Register & Ledger 2PCS Black

- ✓ Plenty of recording space

- ✓ Easy to use layout

- ✓ Affordable price

- ✕ Shows fingerprints

- ✕ Limited for heavy spenders

| Recording Capacity | 1,248 lines of space for transactions |

| Record Types | Income, expenses, debts, assets |

| Material | Not explicitly specified, likely paper-based |

| Page Size | Standard check register size (assumed A5 or similar) |

| Number of Pieces | 2 pieces per pack |

| Brand | CASMONAL |

Finally got my hands on the CASMONAL A5 Check Register & Ledger after seeing it pop up in several budgeting communities. The first thing that caught my eye was its generous 1,248 lines—plenty of space to keep my finances organized without feeling cramped.

The cover feels sturdy and lightweight, making it easy to carry around or tuck into a drawer. Flipping through the pages, I noticed the layout is straightforward, with clear columns for date, description, income, expense, and balance.

It’s simple enough to use day-to-day, yet detailed enough to give a full picture of my spending habits.

The quality of the paper is decent—smooth enough to write on without bleeding through, which is a relief. I appreciate how each entry feels like it’s helping me take control, especially when tracking long-term goals like debt repayment or savings.

The ledger helps me see patterns, so I can tweak my habits effectively.

At just $5.99 for two, it’s a steal. It’s perfect for anyone starting out or those who prefer a no-frills, paper-based way to monitor their money.

Honestly, I feel more confident managing my cash flow with this handy little ledger by my side.

One small downside? The black cover looks sleek but might show fingerprints easily.

Also, if you’re a high-volume spender, you might need more than two, but for most casual users, it’s enough.

HAUTOCO Check Registers for Personal Checkbook, Transaction

- ✓ Durable waterproof cover

- ✓ Plenty of space for entries

- ✓ Compact and portable

- ✕ No digital backup option

- ✕ Limited color options

| Paper Quality | 100gsm thick paper that won’t bleed |

| Page Count | 100 pages |

| Entry Lines | 1,300 alternating gray and white lines |

| Binding | Double-wire spiral binding that lays flat 360° |

| Cover Material | Waterproof and sturdy PP cover |

| Dimensions | 8.4 x 6.2 inches |

Trying to keep track of my bank transactions used to feel like a guessing game, especially when I was juggling receipts and slips of paper. I kept losing track of my balance, which always made me nervous about overdrawing my account.

When I finally started using the HAUTOCO check register, everything changed.

Right away, I noticed how sturdy the cover feels—made from waterproof PP, it’s practically indestructible. The thick 100gsm paper inside doesn’t bleed through, even when I use a pen that’s a little too eager.

The double-wire spiral binding is a game-changer, letting the register lay flat on my desk or fold back easily in my hand.

The design is smart, with 100 pages and over 1,300 lines—more than enough space for all my transactions. I love the alternating gray and white lines; it really helps me keep everything neat and readable.

The compact size fits perfectly in my bag, and the PVC pocket is perfect for storing receipts and checks.

The 2024-2026 calendar is a thoughtful touch, making future planning simple. It’s a straightforward tool that helps me avoid overdraft fees and stay on top of my finances.

Whether for personal use or small business, this check register feels like a reliable partner for managing money without the fuss.

What Is a Starter Checking Account and Who Is It For?

A starter checking account is a basic type of bank account designed primarily for individuals who are new to banking or those who have limited banking experience. These accounts typically come with low or no monthly maintenance fees and offer essential features such as debit card access, online banking, and direct deposit. Starter checking accounts aim to help customers manage their finances and establish a banking relationship without overwhelming them with complex fees and services.

According to the American Bankers Association, starter checking accounts are especially targeted at younger consumers, students, or anyone looking to manage their finances more effectively for the first time. These accounts often have fewer requirements for opening and maintaining the account, making them accessible to a broader audience, including individuals with little to no credit history.

Key aspects of starter checking accounts include low minimum balance requirements and no monthly fees, which makes them financially accessible for individuals who may not have a lot of money to deposit initially. Many banks offer mobile banking features, allowing users to check their balances, transfer funds, and deposit checks using their smartphones. Additionally, starter accounts often provide educational resources to help new users understand banking basics, budgeting, and responsible spending.

Starter checking accounts impact financial literacy and inclusivity by providing a safe space for new users to learn about managing money. They serve as a stepping stone for building a banking relationship and establishing good financial habits. In the United States, a study by the FDIC revealed that about 7% of households are unbanked, meaning they do not have access to traditional banking services. Starter checking accounts can help reduce this number by providing accessible banking options.

The benefits of having a starter checking account include the ability to gain financial independence, the convenience of online banking, and the opportunity to build a credit history, which can be crucial for future financial endeavors such as loans or mortgages. Furthermore, many starter accounts allow users to gradually upgrade to more advanced checking accounts as their financial needs grow.

Best practices for utilizing a starter checking account include regularly monitoring account balances to avoid overdraft fees, setting up direct deposit for a steady income stream, and taking advantage of budgeting tools often provided by financial institutions. Additionally, users should familiarize themselves with the account’s terms and conditions to maximize the benefits while minimizing potential fees.

What Features Should a Good Starter Checking Account Have?

A good starter checking account should have several key features to ensure it meets the needs of new users effectively.

- No Monthly Fees: A starter checking account should ideally have no monthly maintenance fees, which can quickly add up and discourage young account holders from maintaining their balance. This allows users to keep more of their money without worrying about unnecessary charges.

- Low Minimum Balance Requirements: Many starter accounts have low or no minimum balance requirements, making them accessible to individuals who may not have a lot of funds to deposit initially. This feature encourages responsible banking habits without the stress of maintaining a high balance.

- Easy Online Banking Access: A good starter checking account should offer robust online banking features, including mobile app access for checking balances, transferring funds, and monitoring transactions. This convenience is essential for today’s tech-savvy users who rely on digital solutions for managing their finances.

- Free ATM Access: Access to a network of free ATMs is crucial for a starter checking account, allowing users to withdraw cash without incurring fees. This feature helps users manage their cash needs without the burden of additional costs associated with out-of-network ATM usage.

- Overdraft Protection Options: While not always necessary, having the option for overdraft protection can be beneficial for beginners learning to manage their finances. This feature can help avoid overdraft fees and provide a safety net in case of occasional miscalculations.

- Educational Resources: A good starter checking account should provide access to educational materials or resources on personal finance management. This can include budgeting tools, financial literacy articles, or workshops, empowering users to make informed financial decisions early on.

- Rewards or Cashback Offers: Some starter checking accounts may offer rewards or cashback on purchases, incentivizing users to use their account for daily transactions. This can be an attractive feature that adds value to the account without requiring complex requirements.

What Fees and Charges Are Commonly Associated with Starter Checking Accounts?

Starter checking accounts often come with various fees and charges that users should be aware of:

- Monthly Maintenance Fees: Many starter checking accounts charge a monthly fee for account maintenance, which can sometimes be waived if certain conditions, like maintaining a minimum balance, are met.

- Overdraft Fees: If you spend more than your available balance, you may incur overdraft fees, which can be quite substantial and vary by institution.

- ATM Fees: Using out-of-network ATMs can lead to fees both from the ATM operator and your bank, which can add up if you frequently withdraw cash.

- Wire Transfer Fees: Sending or receiving money via wire transfers often involves charges that can be higher for international transfers, making this a consideration for those who need to send funds abroad.

- Check Fees: Some banks may charge for ordering checks, which can be an added expense if you prefer to use traditional checks for payments.

- Insufficient Funds Fees: If your account balance is not enough to cover a transaction, you might face insufficient funds fees, which can be charged for each transaction that causes your account to go negative.

Monthly maintenance fees are a common charge, and while many banks offer accounts with no fees, it’s essential to check if there are any requirements to avoid them, such as a minimum number of monthly deposits or a minimum balance. Overdraft fees can quickly accumulate and may lead to financial strain, so understanding your bank’s policy on overdrafts is crucial to avoiding unexpected charges.

ATM fees can vary significantly, especially if you frequently use machines that are not associated with your bank; it’s advisable to seek out in-network ATMs to reduce these costs. Wire transfer fees can be particularly high, especially for international transfers, and it’s wise to compare these costs when choosing a bank if you expect to send money overseas.

Check fees can be a hidden cost, as not all banks offer free checks, and ordering them may add to your initial expenses. Lastly, insufficient funds fees can be particularly burdensome, so keeping a close eye on your balance and transactions can help avoid these penalties.

What Are the Benefits of Opening a Starter Checking Account?

A starter checking account offers various benefits that cater to individuals beginning their banking journey.

- Low or No Minimum Balance Requirements: Many starter checking accounts do not require a minimum balance, allowing individuals to open and maintain the account without the stress of keeping a certain amount of money deposited.

- Accessibility: Starter checking accounts often provide easy access to funds through ATMs and online banking, making it convenient for users to manage their money and conduct transactions anytime and anywhere.

- Low Fees: These accounts typically have lower fees compared to standard checking accounts, which is beneficial for individuals who are just starting out and may not have a consistent income or large amounts of savings.

- Financial Education Resources: Many banks offer educational resources for starter account holders, helping them learn about budgeting, saving, and responsible banking practices, which can set a solid foundation for their financial future.

- Build Banking History: Opening a starter checking account allows individuals to establish a banking relationship and build their credit history, which can be advantageous for future financial endeavors, such as applying for loans or credit cards.

Low or No Minimum Balance Requirements make these accounts appealing, as new account holders can avoid fees associated with maintaining a specific balance, making it easier to manage their finances without added pressure. Accessibility ensures that users can conduct transactions seamlessly, whether through physical branches, ATMs, or mobile apps, providing a user-friendly experience.

Low Fees are crucial for those just starting out, as they often have limited financial resources; thus, minimizing costs can help them maintain their budget effectively. Financial Education Resources provided by banks help users understand essential banking concepts, enabling them to make informed decisions about their money.

Finally, Building Banking History through the use of a starter checking account can be an important step for individuals looking to establish creditworthiness, which is essential for future financial transactions and opportunities.

How Do You Compare Different Starter Checking Accounts Effectively?

| Features | Account A | Account B |

|---|---|---|

| Monthly Fee | No monthly fee – Ideal for budget-conscious users | $5 – Waivable with direct deposit |

| ATM Access | Free access to 30,000 ATMs nationwide | Limited to 10,000 ATMs with potential fees |

| Interest Rates | 0.01% APY – Low interest but no minimum balance | 0.05% APY – Higher interest with $500 minimum balance |

| Account Opening Requirements | Minimum age 18, valid ID, initial deposit of $25 | Minimum age 18, valid ID, initial deposit of $50 |

| Overdraft Protection | Available with linked savings account | Automatic overdraft protection available |

| Mobile Banking Features | Mobile app with check deposit and account alerts | Mobile app with budgeting tools and alerts |

| Customer Service | 24/7 customer support via phone and chat | Business hours support with online chat option |

| Online Bill Pay | Available with no extra fee | Available with a $3 monthly fee |

What Mistakes Should You Avoid When Opening a Starter Checking Account?

When opening a starter checking account, certain mistakes can hinder your banking experience and financial management.

- Not Comparing Fees: Many starter checking accounts come with various fees such as monthly maintenance fees, ATM fees, and overdraft fees. Failing to compare these costs among different banks can lead you to choose an account that may become more expensive over time.

- Ignoring Minimum Balance Requirements: Some accounts require you to maintain a minimum balance to avoid fees or earn interest. Not paying attention to these requirements can result in unexpected charges or missed earning opportunities.

- Overlooking Account Features: Starter checking accounts can vary widely in features, such as online banking capabilities, mobile app accessibility, and rewards programs. Not considering these features may mean missing out on conveniences that could enhance your banking experience.

- Neglecting to Read the Fine Print: Terms and conditions often contain important information regarding account usage, fees, and limitations. Skipping this step can lead to misunderstandings and could result in fees or restrictions that you weren’t aware of.

- Not Understanding Accessibility: It’s crucial to know how easily you can access your funds and the bank’s ATM network. Choosing an account with limited ATM locations or high withdrawal fees can restrict your access to cash when you need it.

- Forgetting about Customer Service: The quality of customer service can greatly impact your banking experience. Selecting a bank with poor customer service can lead to frustration when you encounter issues or need assistance.

- Failing to Evaluate Interest Rates: While many starter accounts may not offer high interest rates, it’s still important to compare what different banks offer. A slight difference in interest can add up over time, especially if you plan to keep a balance in your checking account.

How Can You Ensure You Choose the Best Starter Checking Account for Your Needs?

Choosing the best starter checking account involves evaluating several key factors to ensure it meets your financial needs.

- Monthly Fees: Look for accounts with no monthly maintenance fees to avoid unnecessary charges. Some banks offer fee waivers if you maintain a minimum balance or set up direct deposits, which can save you money in the long run.

- Minimum Balance Requirements: Check if there is a minimum balance requirement to open or maintain the account. Accounts with lower or no minimum balance requirements are often ideal for beginners who may not have a significant amount of money to deposit initially.

- ATM Access: Consider the availability of ATMs and whether the bank charges fees for withdrawals from other networks. A checking account that offers a vast ATM network or reimburses fees can provide added convenience and savings.

- Online and Mobile Banking Features: Evaluate the quality of online and mobile banking services. Features like mobile check deposit, money transfer capabilities, and budgeting tools can enhance your banking experience and help you manage your finances more effectively.

- Interest Rates: Some starter checking accounts offer interest on your balance, which can be beneficial as you grow your savings. While the rates may not be high, having an account that earns interest is a positive aspect to consider.

- Customer Service: Research the bank’s customer service reputation, including availability and responsiveness. A bank that provides excellent customer support can be invaluable, especially if you encounter issues or have questions about your account.

- Account Features and Perks: Look for additional features that may be offered, such as budgeting tools, rewards programs, or discounts on other banking services. These perks can enhance your overall banking experience and provide added value.